Do you remember when the last player repeated the message - it was completely different than the original message!!

The first reverse mortgage loan was closed in 1989. Since that time there has been a lot of "campfire" activity with regard to myths and erroneous information that has circulated with this product. Here are some of the more common ones:

Myth #1: The lender or government will own your home.

False -With a reverse mortgage loan, you, your family and/or your estate continue to retain ownership of your home. The lender does not take control of the title. The lender's interest is limited to the outstanding loan balance as a lien on title.

Myth #2: The reverse mortgage requires that I make monthly payments.

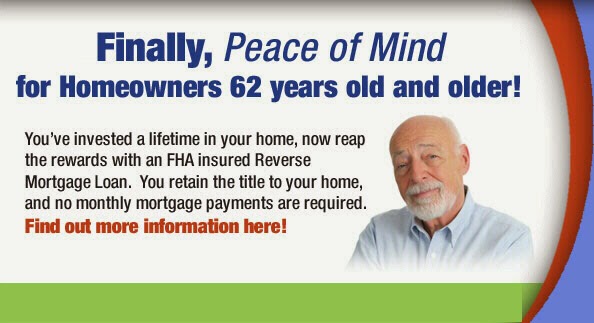

False - There are no monthly payments required to your lender, however, the borrower is responsible for payment of all property taxes, insurance, and general upkeep of the home.

Myth #3: My children will be held responsible for the repayment.

False - The reverse mortgage is a non-recourse loan. This means that the lender can only derive repayment of the loan from the proceeds of the sale of the property. Even if the value of the home is reduced due to economic, market or property perils, you or your estate can never owe more than the value of the home. Although your heirs will not be responsible for repayment, they are able to work with the loan servicer to repay the loan and as an option buy the home for themselves.

Housing prices were up in April, and sales blew past economists expectations, but inventory continues to be tight.

Housing prices were up in April, and sales blew past economists expectations, but inventory continues to be tight. You can now find pricing that includes all the third party fees most lenders and quote websites leave out.

You can now find pricing that includes all the third party fees most lenders and quote websites leave out.

The first reverse mortgage loan was closed in 1989. Since that time there has been a lot of "campfire" activity with regard to myths and erroneous information that has circulated with this product. Here are some of the more common ones:

The first reverse mortgage loan was closed in 1989. Since that time there has been a lot of "campfire" activity with regard to myths and erroneous information that has circulated with this product. Here are some of the more common ones: